For most of my working life, fusion was something that happened inside national laboratories. It was funded by governments, measured in decades, and defended — when it needed defending — on the grounds that the physics was worth knowing. I spent those years on ADITYA and on SST-1 at the Institute for Plasma Research, and before that at Saha Institute, on India’s first tokamak. Nobody in that world used the word “market.”

That world has changed, and the Fusion Industry Association’s 2026 survey documents the change with unusual clarity. It is worth reading carefully, and it is worth reading in India.

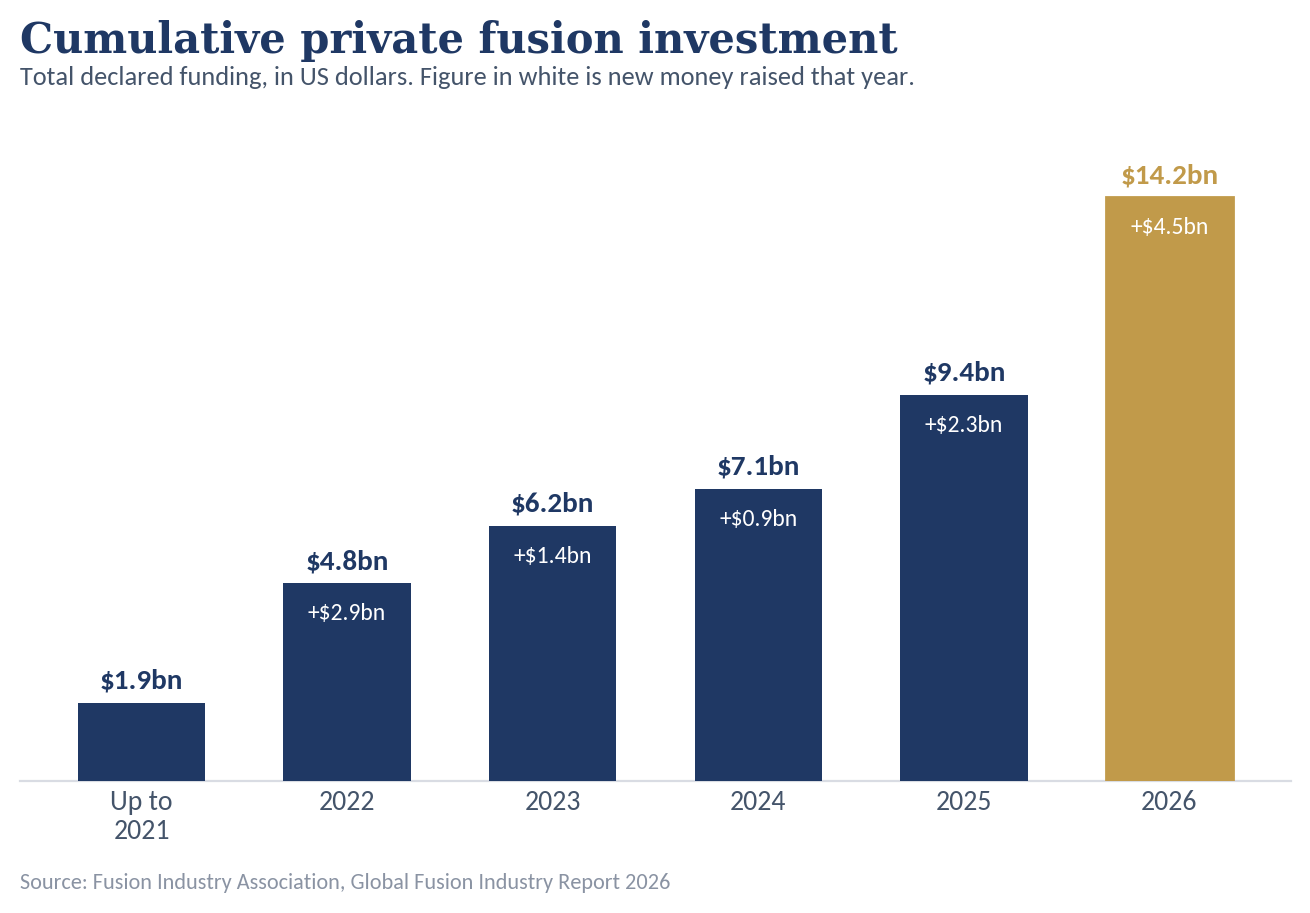

The FIA’s 2026 report counts 56 private fusion companies worldwide and $14.24 billion in cumulative declared funding. Of that, $4.48 billion arrived in the last twelve months alone — more than any single government’s fusion budget over the same period.

The numbers

In 2021, when the FIA published its first survey, the sector had attracted under $2 billion, with 85% of it concentrated in four companies. That is roughly a 650% increase in five years, and the concentration has broken up: five companies have now crossed $1 billion individually, and dozens of others have raised meaningfully.

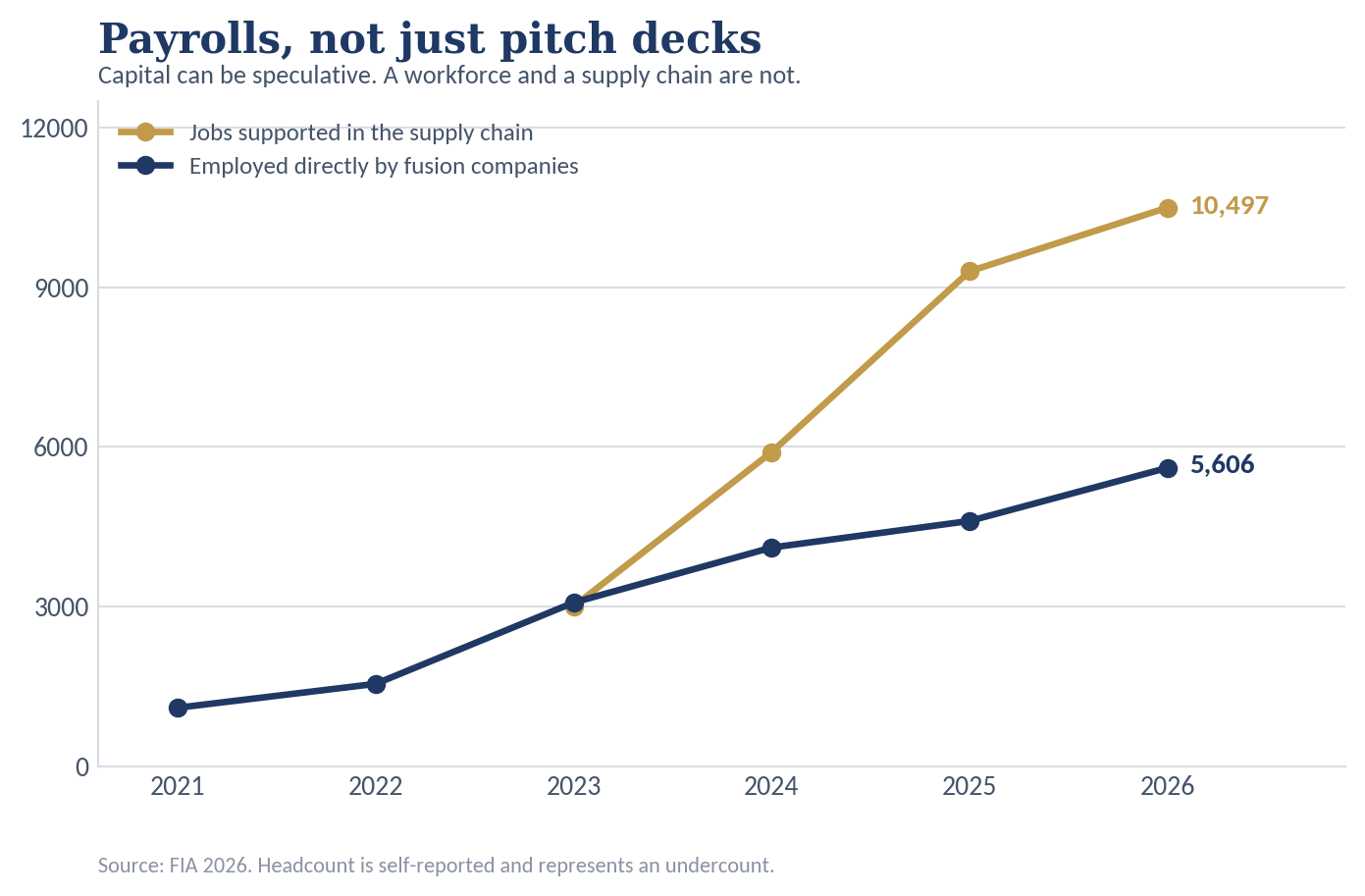

The workforce numbers are, to my mind, the more telling indicator. Fusion companies now directly employ over 5,600 people (and the FIA notes this is an undercount), supporting an estimated 10,497 supply-chain jobs. Capital can be speculative. Payrolls and purchase orders are not. A supply chain is forming — magnets, cryoplant, tritium handling, high-power RF, precision fabrication — and it is forming in specific countries.

What is actually driving this

Three things have changed since 2021, and only one of them is physics.

First, the demand side found fusion before fusion found the grid. Environmental urgency and energy security were always the arguments. The new argument is the electricity appetite of artificial intelligence. Hyperscalers building frontier models are discovering that compute is, in the end, a power problem. The FIA report captures the consequence: for the first time, it asked companies about commercial agreements, and six already hold siting agreements for a commercial plant with four more evaluating options, while five have a power purchase or offtake commitment with two in discussion. When a buyer signs for electricity that does not yet exist, the risk calculus of the entire sector shifts.

Second, revenue has stopped being something that waits for the power plant. A number of companies in the survey are monetising fusion-adjacent capability today — medical isotopes, neutron radiography, radiation-effects testing, materials qualification, boron neutron capture therapy. SHINE, Astral Systems and TAE’s life-sciences arm are the clearest examples. This is not a distraction from fusion energy; it is how the intermediate decade gets financed, and it is how an engineering team learns to operate real hardware under real regulation before it is asked to operate a power plant.

Third, the industry is entering the public markets. Two fusion companies are in the process of listing through mergers. That will bring capital, and it will bring a discipline that fusion has never faced: quarterly scrutiny, and consequences for missed milestones.

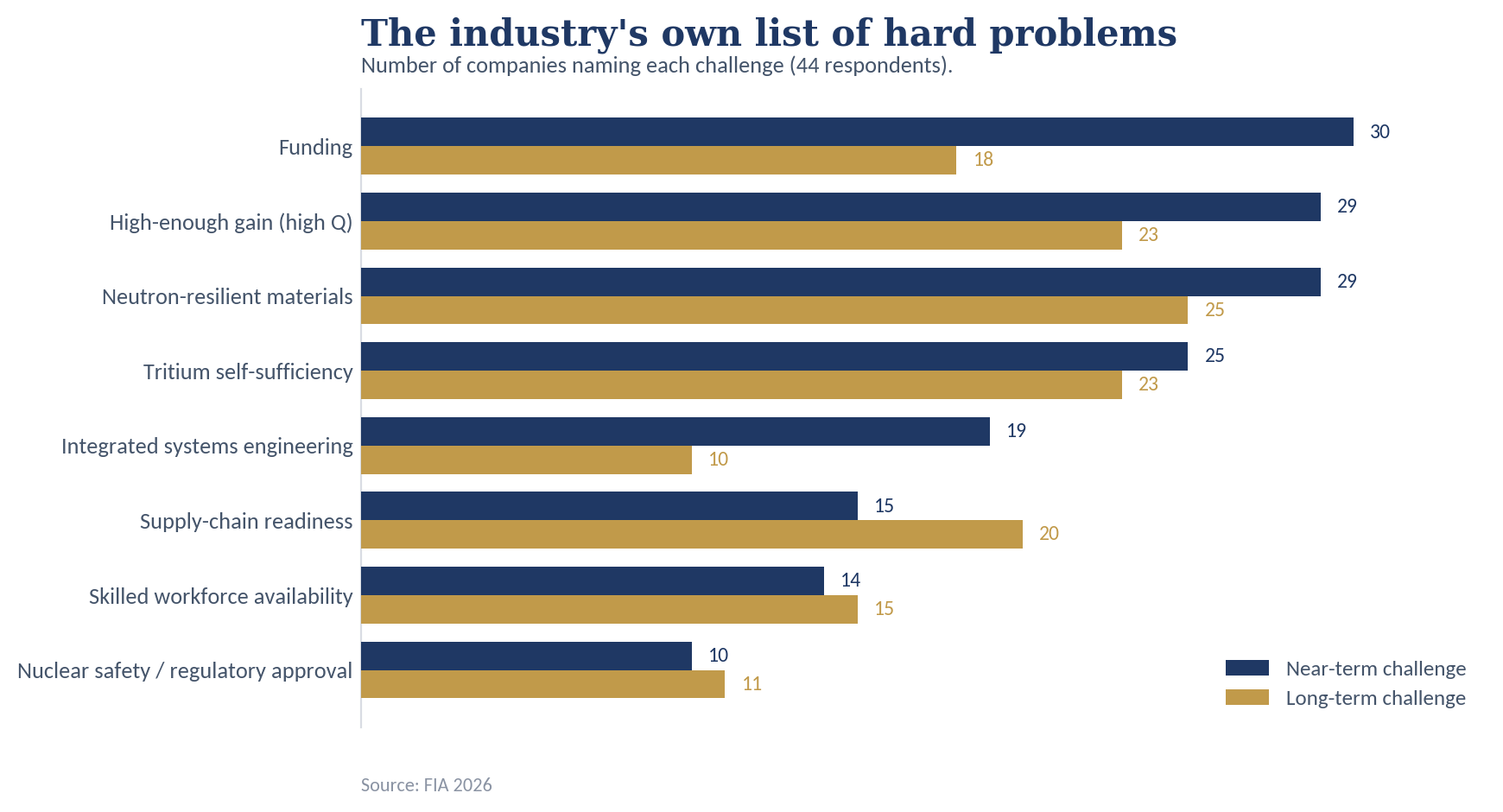

None of this means the hard problems have gone away. The same survey asks companies to name their challenges, and the answers are sober: funding, achieving high enough Q, neutron-resilient materials, tritium self-sufficiency, supply-chain readiness for specialised components. These are unsolved. Companies that pretend otherwise will be found out, and the market — which the FIA rightly calls a harsher peer reviewer than any journal — will find them out quickly.

Where India stands in this picture

The FIA report tracks three Indian companies — in Gandhinagar, Bengaluru and Hyderabad. That is real, and it is new; two years ago there were none. India now appears on the map of private fusion alongside the United States, Germany, Japan, the UK and China.

The three in the survey are not, in fact, the whole of it. The FIA’s data comes from companies that respond to it, and its authors are candid that this produces an incomplete picture — they say as much about China. The same is true of India: there are a few more early-stage fusion ventures here that do not appear in this year’s report. The domestic ecosystem is somewhat larger than the survey shows, and it is growing. That is worth saying plainly, because the numbers below understate us.

Even so, the capital gap is stark. Set the declared funding of India’s private fusion sector against $14.24 billion raised globally and our share does not register as a rounding error — it is a fraction of one percent, in a country that is one-sixth of humanity and among the fastest-growing electricity markets on earth. Individually, our companies are operating on budgets that several of the survey’s participants would classify as a single line item. That gap is the whole story.

It is not a gap of talent, and it is not a gap of institutional depth. It is a gap of capital formation and enabling machinery — and both are fixable.

The Indian companies in the survey are doing serious work — a privately built low-aspect-ratio tokamak commissioning toward first plasma, indigenous HTS magnet development, laser-driven inertial confinement. And IPR, BARC, the DAE laboratories and the IITs represent decades of accumulated plasma, materials and nuclear engineering capability that most countries cannot match. India built ADITYA and SST-1 on its own.

What moving fast would actually mean

I would offer four propositions, in order of urgency.

1. Regulatory clarity is worth more than subsidy. The SHANTI Act, 2025 opened nuclear energy to private participation, and that was the necessary precondition for everything else. But the Act was drafted around fission, and fusion devices sit awkwardly inside its definitions. A non-power neutron source, a fusion power plant, and a sub-critical fusion-fission hybrid are three different hazard profiles requiring three different regulatory treatments. What the sector needs is not light-touch regulation — the hazards are real, and anyone working with tritium, activated materials, beryllium, superconducting magnets and high voltage should say so plainly. What it needs is proportionate regulation: an express statutory category for fusion energy facilities, with siting and licensing conditions derived from a facility-specific source-term analysis rather than inherited from the fission template. The UK’s Energy Act 2023 and the US NRC’s byproduct-material approach are useful precedents, not because they are lenient, but because they are specific. A clear, predictable licensing pathway is the single cheapest thing the state can provide, and it is the thing investors ask about first.

2. Public-private instruments, not just public money. Sixteen companies in the FIA survey report cost-shared public-private partnerships. The two most frequently cited are the US DOE’s Milestone-Based Fusion Development Program and INFUSE, which gives companies competitive access to national-laboratory expertise and facilities. Both are structurally simple and both are replicable here. India already has the ingredients — ANRF, the RDI Fund, TDB — and it already has the national assets that private teams cannot build for themselves: test facilities, computational infrastructure, tritium and materials expertise, and above all people. A milestone-linked, cost-shared instrument that lets private teams buy structured time on DAE and IPR capability would move Indian fusion further than a grant of the same size.

3. Build the supply chain deliberately. REBCO tape, cryoplant, high-power gyrotrons and neutral beam systems, tritium-compatible components — these are the choke points, and the FIA respondents name supply-chain readiness as both a near-term and a long-term challenge. Whoever manufactures these components will capture a large share of the value of fusion regardless of whose reactor design wins. India has a genuine industrial opening here, and it is available now, years before anyone sells a fusion electron.

4. Take the intermediate markets seriously — India needs them anyway. Fusion-adjacent neutron sources produce things this country is short of: medical radioisotopes for cancer therapy and diagnostics, non-destructive testing capability for aerospace and battery manufacturing, materials qualification under fast neutrons. These are not consolation prizes. They are markets with patients and customers today, they generate revenue that funds the harder physics, and they force a young industry to learn safety culture and regulatory practice on smaller machines. India is a large, price-sensitive, underserved market in precisely these areas. The intermediate step is not a detour; for a capital-constrained ecosystem, it may be the only viable road.

A word about promises

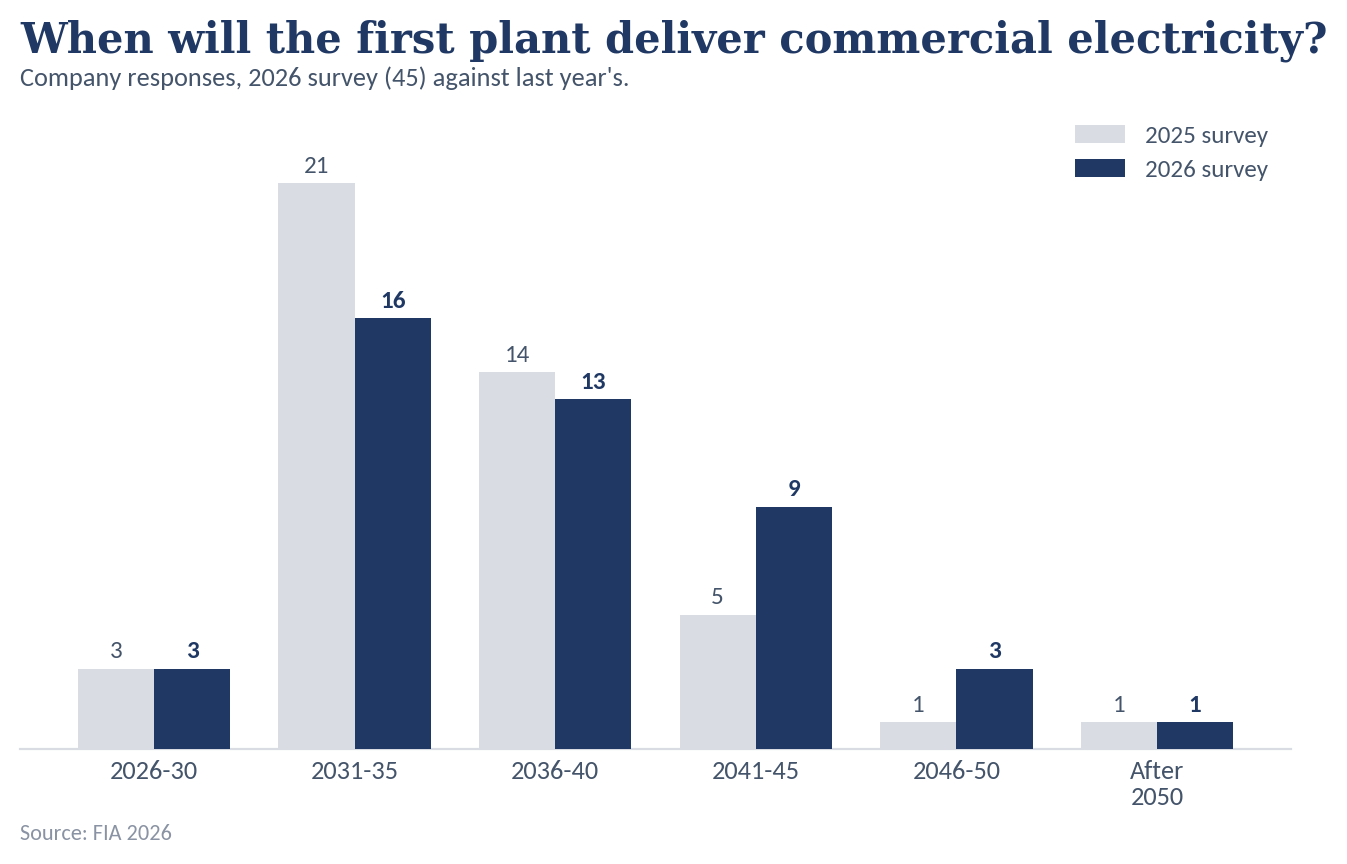

The FIA notes that most companies still expect commercial fusion electricity in the 2030s, and that these timelines have held steady across five surveys. I would ask Indian readers — and Indian investors — to hold two thoughts at once.

The first is that fusion is now a legitimate investment domain, with real customers, real supply chains and real capital, and that a country which stays out of it for another five years will be buying the technology rather than building it.

The second is that anyone in India who promises you a fusion power plant in seven years is not being straight with you. The honest position is that the physics is hard, the materials are harder, the tritium cycle is harder still, and that the credible near-term value lies in neutrons, isotopes and industrial capability — with electricity as the destination, not the first stop. Credibility with DAE, with BARC, with the regulator and with patients is built by not over-promising. It is the only currency a young industry actually has.

India has the scientific base. It now has the legal opening. What it does not yet have is capital at scale, a fusion-specific regulatory category, or a public-private instrument that lets private teams stand on the shoulders of the national programme rather than duplicate it.

None of those is a hard problem. They are decisions. And the FIA’s numbers suggest we have perhaps three to five years to take them.